Posted by Mary Milorrie Campos

Dec 16, 2021

Share

The Financial Accounting Standards Board (FASB) pushed through with the implementation of the new lease accounting standards (ASC 842) for private companies after a two-year delay.

Private entities with existing leases should double their efforts to amend their system and internal controls to properly adopt the new leasing standard.

(Note: Countries conforming to the International Financial Reporting Standards (IFRS) follow a different lease standard called IFRS 16. Though ASC 842 and IFRS 16 are similar in nature, they also have their differences.)

In its earlier document, the FASB required private entities to comply with the new standard as early as the fiscal years beginning 15 December 2019. However, this deadline has been pushed forward when the standard-setting body voted for its deferral.

Come 2020, the FASB has postponed its implementation again for another year due to COVID-19. However, it rejected further appeals to extend its effective date for two years.

For the fiscal period beginning after 15 December 2021, private entities in the U.S. must include all lease obligations in their financial statements. The interim period is within the fiscal year beginning after 15 December 2022.

Here are some of the basic information to know about the new lease accounting standards.

What is a lease?

In its Accounting Standards Update 2016-02 (PDF, 856 KB), FASB defines a lease as:

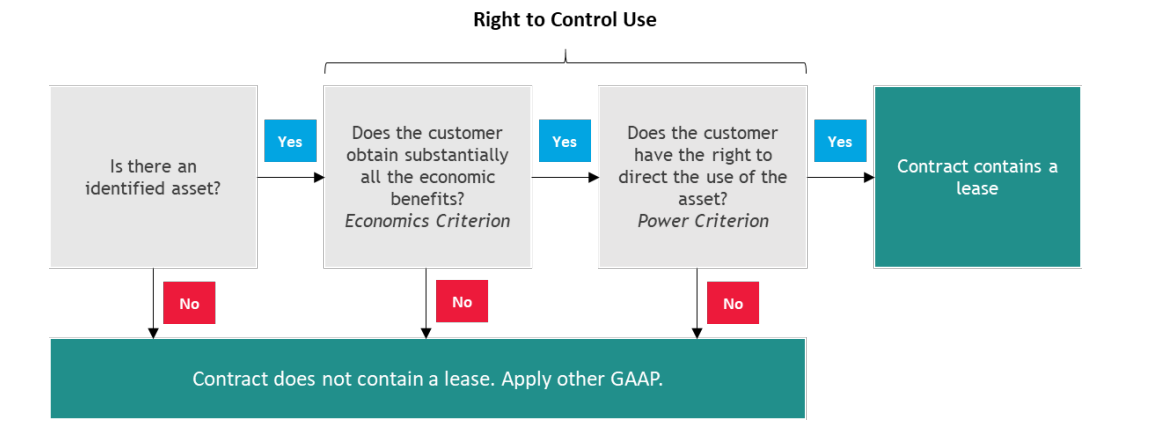

“A contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.”

An entity has control over the use of the identified asset if it has:

- the right to acquire all economic benefits of using the asset, and

- the right to direct the use of the asset.

This flowchart provides an easy way to determine if the contract contains a lease.

Source: Accounting for Leases: Identifying a Lease (BDO United States, October 2021)

Lease classification

Under the new rule, private entities must account for two types of leases:

-

Finance lease (formerly called capital lease)

A finance lease is a type of commercial lease wherein the lessee becomes the owner of the leased asset before the lease arrangement expires. It should meet any of the following criteria:

- The lessee acquires ownership of the underlying asset by the end of the lease term.

- The lessee has the option to purchase the underlying asset that is reasonably certain to be exercised.

- The lease term exceeds 75% of the asset’s economic life. But if the commencement date falls at or around the end of the economic life, this criterion can’t be used in classifying the lease.

- The present value of all lease payments and any residual value of the underlying asset is equal to or has exceeded greatly all fair value of the underlying asset.

- The underlying asset should be specialized to the extent that the lessor has no alternative use to it at the end of the lease term.

If the lease didn’t meet any of the above criteria, it will be considered an operating lease by the lessee.

-

Operating lease

An operating lease is a type of contract that allows the use of an asset without transferring its ownership rights to the lessee. Examples are rented buildings and other properties with long lifespans like office equipment, aircraft, and machinery.

Changes to lease accounting

The defunct ASC 840 allows organizations to exclude operating leases in financial statements. They can opt to disclose it to the footnotes of their report instead of reporting it alongside other liabilities. However, this method makes this liability almost invisible, creating ambiguity to the company’s actual financial position. This is the reason why FASB implemented the amendments.

Under the new guidance, lessees conforming to the Generally Accepted Accounting Principles (GAAP) must recognize both lease assets and lease liabilities for all leases. This means they must record both finance and operating leases on their balance sheet rather than excluding the latter.

Through this, the FASB expects to increase transparency into how public and private entities report their leasing obligations to their financial statements.

Separating components

The ASC 842 also expands its guidance in identifying and separating the lease and non-lease components in the contract. As such, entities should account for lease components using the new lease accounting guidance. For non-lease components, the relevant GAAP rule should apply.

Paragraph 842-10-15-27 sets down the criteria for separating a lease component. As a start, an entity can ask themselves the following questions:

- Do I benefit from the right of use of the asset, including the other readily available resources available to me?

- Is my right of use neither highly dependent on nor highly interrelated with my other rights to use underlying assets in the contract?

If the entity answered yes to both questions, then the asset is likely to be a lease component.

In addition, the component of a contract must be limited to “items or activities that transfer a good or service to the lessee,” paragraph 842-10-15-27 states. This means administrative tasks in setting up a contract or initiating a lease that does not transfer a good or service to the lessee is not considered a component of the contract. The same goes for the reimbursement or payment of the lessor’s costs.

What should private companies do?

Complying with ASC 842 is a time-consuming process. The two-year delay may have provided extra time to businesses, but the road is still long for companies that can’t be bothered in implementing it, especially during the pandemic.

One of the initial steps to consider at the beginning of the compliance is to form an implementation team that would take charge of the process — from evaluation leases to adopting the new standard.

It’s also critical to communicate with all stakeholders about its possible effects on the company’s financial statements.

If the organization still uses Microsoft Excel in accounting for leases, it’s time to consider investing in a software solution. The more leases a company has, the longer it will take to comply with the new standard. The dashboard and reporting features of a software solution can help them organize their leases faster.

Get the help you need

Do you need additional manpower to comply with ASC 842? D&V Philippines can provide you with reliable back-office support. Contact us today to learn more about our services. You can also read our whitepaper, Finding the Right Talents: D&V Philippines’ Solutions to Modern Accounting Firms, for more information.